Before I begin, please note: I hated this chapter. If there are any errors please let me know asap!

A deductible

Definitions:

- Payment per Loss:

- Limited Payment per Loss:

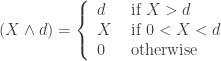

Expected Values:

![\begin{array}{rll} E[(X-d)_+] &=& \displaystyle \int_{d}^{\infty}{(x-d)f(x)dx} \\ \\ &=& \displaystyle \int_{d}^{\infty}{S(x)dx} \end{array}](https://s0.wp.com/latex.php?latex=%5Cbegin%7Barray%7D%7Brll%7D+E%5B%28X-d%29_%2B%5D+%26%3D%26+%5Cdisplaystyle+%5Cint_%7Bd%7D%5E%7B%5Cinfty%7D%7B%28x-d%29f%28x%29dx%7D+%5C%5C+%5C%5C+%26%3D%26+%5Cdisplaystyle+%5Cint_%7Bd%7D%5E%7B%5Cinfty%7D%7BS%28x%29dx%7D+%5Cend%7Barray%7D&bg=ffffff&fg=333333&s=0&c=20201002)

![\begin{array}{rll} E[(X\wedge d)] &=& \displaystyle \int_{0}^{d}{xf(x)dx +dS(x)} \\ \\ &=& \displaystyle \int_{0}^{d}{S(x)dx} \end{array}](https://s0.wp.com/latex.php?latex=%5Cbegin%7Barray%7D%7Brll%7D+E%5B%28X%5Cwedge+d%29%5D+%26%3D%26+%5Cdisplaystyle+%5Cint_%7B0%7D%5E%7Bd%7D%7Bxf%28x%29dx+%2BdS%28x%29%7D+%5C%5C+%5C%5C+%26%3D%26+%5Cdisplaystyle+%5Cint_%7B0%7D%5E%7Bd%7D%7BS%28x%29dx%7D+%5Cend%7Barray%7D&bg=ffffff&fg=333333&s=0&c=20201002)

We may also be interested in the payment per loss, given payment is incurred (payment per payment)  .

.

.By definition:

![E[X-d|X>d] = \displaystyle \frac{E[(X-d)_+]}{P(X>d)}](https://s0.wp.com/latex.php?latex=E%5BX-d%7CX%3Ed%5D+%3D+%5Cdisplaystyle+%5Cfrac%7BE%5B%28X-d%29_%2B%5D%7D%7BP%28X%3Ed%29%7D&bg=ffffff&fg=333333&s=0&c=20201002)

Since actuaries like to make things more complicated than they really are, we have special names for this expected value. It is denoted by  and is called mean excess loss in P&C insurance and

and is called mean excess loss in P&C insurance and  is called mean residual life in life insurance. Weishaus simplifies the notation by using the P&C notation without the random variable subscript. I’ll use the same.

is called mean residual life in life insurance. Weishaus simplifies the notation by using the P&C notation without the random variable subscript. I’ll use the same.

and is called mean excess loss in P&C insurance and is called mean residual life in life insurance. Weishaus simplifies the notation by using the P&C notation without the random variable subscript. I’ll use the same.Memorize!

- For an exponential distribution,

- For a Pareto distribution,

- For a single parameter Pareto distribution,

Useful Relationships:

![\begin{array}{rll} E[X] &=& E[X\wedge d] + E[(X-d)_+] \\ &=& E[X\wedge d] + e(d)[1-F(d)] \end{array}](https://s0.wp.com/latex.php?latex=%5Cbegin%7Barray%7D%7Brll%7D+E%5BX%5D+%26%3D%26+E%5BX%5Cwedge+d%5D+%2B+E%5B%28X-d%29_%2B%5D+%5C%5C+%26%3D%26+E%5BX%5Cwedge+d%5D+%2B+e%28d%29%5B1-F%28d%29%5D+%5Cend%7Barray%7D&bg=ffffff&fg=333333&s=0&c=20201002)

Actuary Speak (important for problem comprehension):

- The random variable

is said to be shifted by

is called mean excess loss or mean residual life.

- The random variable

can be called limited expected value, payment per loss with claims limit, and amount not paid due to deductible.

- If data is given for

with observed values and number of observations or probabilities, the data is called the empirical distribution. Sometimes empirical distributions may be given for a problem, but you are still asked to assume an parametric distribution for